Thousands of business owners are expected to retire over the next decade or so. Most do not have an exit strategy. We will explore options and solutions.

Recently, SCORE, the premier organization of volunteer business mentors, published an infographic outlining the results of a retirement survey among small business owners. Unfortunately, it reveals an alarming lack of readiness. The smaller the business, the more exit planning is lacking.

A lot of retirements are involuntary and sudden. For this reason, it is essential to get this started early so there is a plan for the survival not only of the business, but more importantly for your family and anyone else who depend on your ability to run it.

The research reveals that four out of ten are not sure that they will be able to retire by age 65. Three of them do not have retirement savings outside the business at all. Two of them expect the sale of the business to provide the funds for their retirement. That is seriously disturbing because other research shows that not only do they not have an accurate picture of the value, their expectations are usually grossly exaggerated. The one valuation factor they overlook most often is the fact that they are the business. It cannot run without them and therefore has no value beyond its equipment and inventory.

Of course, you are not one of those people because you have watched the video on this page and read the books I have recommended, right? Business owners are different than other people. They take more risks. They are willing to take a step not knowing exactly where it leads. I get that, but retirement is inevitable. You just don't know when. The good news is that it is one of those things you do have a great deal of control over as long as you get started early.

Timing is definitely a factor when it comes to selling your business and hopefully reap the rewards of your hard work, but this book goes into a lot more detail than just timing.

You will learn how to value your business so you will know precisely how much is available for your retirement. If there is a gap, it also provides a number of things you can do to close it before it is too late.

For most owners, selling their business is an unpleasant task. It is unknown territory and navigating unknown territory requires additional concentration. Unlike familiar territory it requires your full attention all the time.

Another, perhaps even more significant reason it is so hard, could be that it has become a manifestation of unfulfilled dreams and hopes. The life in affluence you imagined turned out to be long hours and family sacrifices. The hobby you once loved became a chore. You have mouths to feed so you hang in there year after year. Even though it is uncomfortable, status quo feels safer than action.

You may seek comfort in an illusion that you have created tremendous value and if you just hang in there long enough things will turn around. You may hold on to this belief until the day the bubble bursts and you are forced to face the truth that your business is just a job like any other job. You are burned out. Maybe your health has taken a toll. Maybe your family life is in shatters and this is what forces you to face the music. Your business is worthless. Who is going to want to buy a job?

When you have arrived at a dark place like that, it is very difficult to muster the energy and enthusiasm it takes to let go of a business that has robbed you of your sweat and tears but given back almost nothing.

It is for this reason exit planning really needs to start the day you open for business. If you start the business from the point of view that you started it to sell it, not to have something to do, not to become wealthy, not to have flexibility in your life or any of the other reasons people give why they wanted to start their own business, then, selling it becomes a day of celebration, the day you reach your goal, the day you cash in.

Three Step Exit Planning

Exit planning starts with setting goals, first for yourself, then for your family and then for anyone else you consider stakeholders in your business.

Getting Yourself Ready

What does a life of joy look like to you? The simple task of establishing that in your own mind could give you a whole new perspective and purpose in life. Of course, no one lives in a vacuum. Our lives are connected with other people around us. How does your dreams align with theirs? Do you have to or are you willing to make any concessions? You may want to live in the country. Your spouse and kids are all city dwellers. How do you reconcile that? You may have employees. How does your departure affect them? Do you care?

Getting Your Business Ready

The second step is to get your business ready. Can it run without you? Why would you want your business to run without you? It may not be important from day one while you are still in building mode, but when the day of selling comes around, independence from you becomes vital. If it cannot exist without you, its only value is in its assets. Therefore, your job is to create transferable value. This means creating a management team, establishing systems and processes and many other things that build value.

Getting Your Buyer Ready

The third step is getting the buyer ready. You may think this is not really your responsibility, but you would be wrong. The more you understand about who the buyer is, what makes him or her happy, the smoother the transition. Once you have vetted and selected a serious buyer, you will go through a time of due diligence. Since you are a stranger to the buyer, he or she is going to verify that the business is as valuable as you say it is. Does it meet her expectations? The better you can understand and anticipate her requirements, the better she will feel. We are not talking about putting lipstick on a pig, but providing actual useful information to support your claims about the business. Many things can go wrong during this time. It is during this time price adjustments may be made and they always make you upset or kill your deal altogether. To avoid that, have good and verifiable documentation ready to counter every argument. Your job is to make it an easy and stress free experience for the buyer. Then, it will be pleasant and stress free for you as well.

Conclusion

If you started your business for the wrong reason, all may not be lost. Barring an emergency exit, every step you can take well in advance will bring you closer to your goal.

When you build your business from day one to sell it instead of to have a job, letting go of it becomes a whole lot easier. It can become downright enjoyable.

Even if you have just realized that selling it could become more challenging that you thought, all may not be lost. There may still be time to build value so you can go do what you really wanted to do in the first place.

Almost half of all business owners believe they have taken all the steps they need to retire or they do not need to do anything. They believe they can exit at any time. Another large group believe exit planning can wait till they are good and ready to exit.

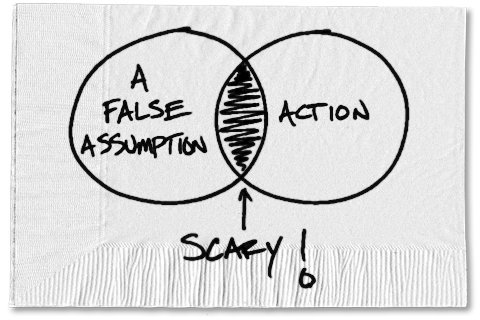

Those are all assumptions that could derail almost any retirement, but it gets worse.

They also frequently make erroneous assumptions about other essential aspects of retirement planning such as the value of their business and how much they can withdraw from retirement funds to support their spending expectation.

Business people are visionaries. They take more risks. They are more optimistic. They are more prone to be in denial when things do not turn out as expected. I get that, but that kind of thinking can be dangerous when it comes to retirement. Let us begin with the business valuation.

Business valuation is not an exact science. When you are not fully engaged in crafting an exit strategy, it is easy to get sucked into believing the shortcuts and rules of thumb perpetuated in 500 word or less blog posts. Valuation is complex. Hundreds of factors go into a professional evaluation and even then, the final court of arbitration is a willing and able actual buyer with checkbook in hand. The rumor that Joe sold his deli for six times EBIDTA does not matter one bit. Yours most likely differs in several significant ways and so will your valuation. Hire a professional business valuation expert.

Do not forget that the sale will trigger capital gains tax and that the rate is likely to be higher than you think. Ask your accountant to calculate and accurately estimate the tax you will have to pay based on the expert valuation.

Since the value of the business is most likely grossly overestimated, your retirement savings may be equally underfunded with the expectation that the sale of the business would make up for it. If that is the case, turning it around could take years, perhaps decades. If that is your situation, planning for your exit when you are ready is much too late. Business owners also frequently overestimate the amount of money they can safely withdraw from their savings. People live longer, health care costs are soaring and conventional wisdom may no longer apply. Talk to your financial adviser. Get an accurate estimate of what you can realistically withdraw from savings.

In addition, a broker will charge in the vicinity of 10 to 12%. Get a detailed description of the services they will provide. Your attorney and accountant will also need to be paid for additional work.

With this information and five to ten years available, it is possible to create an exit plan based on facts, or at least as close to facts as you can get, that will allow you to achieve your retirement goals.

In most cases, it is not the lack of buyers that kill your deal, it is false assumptions about it.

This book does not make you an expert on business valuation. It does not even help get an accurate estimate of the value of your business. What it does do is give you the vocabulary you need to understand what your professional business appraiser is talking about and the method he will be using.

Charlie Whiting, Race Director of Fédération Internationale de l'Automobile (FIA), the governing body of many auto racing events, suddenly died on March 14, 2019 only 66 years old. Mr. Whiting had been involved in motor racing just about as far back as anyone can remember. Although there had been discussions about what the world would look like after Charlie Whiting, nobody had expected it would come this soon and the organization was not prepared for it.

Charlie Whiting Long Term Succession Plan

That is also the case for the vast majority of small and medium size companies in America today. Especially small companies rely on one person to hold everything together. That is not good when disaster strikes and he suddenly goes missing. The result could be devastating for his family and employees. Learn about succession planning and then do something about it.

It is possible to buy insurance for when disaster strikes, but not for when a trusted employee goes to work for a competitor. There is no substitute for a comprehensive succession plan.

Worker cooperatives are less likely to have this problem as they tend to spread the tasks on more shoulders. Because they are owners, they tend to stay longer and are more committed than wage earners. Worker cooperatives are often founded on the idea that we can do more together than we can individually, so business management for them naturally becomes a team effort.

Succession planning is not the same as exit planning. Succession planning is part of an exit plan, but people leave all the time for all kinds of reason. You really need to have a way to respond when they do at all times. You may not get the notice you expected. Disaster could strike at any time. Therefore succession planning should also be part of a comprehensive disaster plan.

As a business owner, you are no doubt used to setting goals and achieving them. Are you as good at it in your personal life? Most people who start a business do it because they have certain goals they want to achieve. Maybe they want to have the flexibility to work when they want. Maybe the motivation is to be able to build extraordinary wealth. Whatever the reason, it is far more difficult to be motivated to set goals for retirement, so only very few have given much thought to that.

Setting Goals for Yourself

This is how important it is to do: You may have about 40 or so years of work life, but you may also have another 40 years in retirement. Sure, you have Social Security, but that may only provide a small fraction of the income you need for the lifestyle you want. Forty years is also a really long time if you have nothing meaningful to do, so setting retirement goals should also have provisions for that.

Setting Goals for You and Your Family

Do not think you are done when you have set goals for yourself. Most likely, you are connected to both an immediate family and an extended family. They may have plans of their own and they may not look like yours. What do you do? You can either try to work it out with them or major upset could result. It is best to prepare for lots of respectful communication.

Do write down your own goals and plans in great detail, but be sure to write anything that is negotiable in pencil. Decide what is non-negotiable and write it with a permanent marker.

The Extended Family

Often times, people beyond the immediate family also have an interest in what you do with your business. Some of them may have expectations that never crossed your mind before. Prepare yourself mentally for surprises; even conflict.

Other Stakeholders

There may be others outside your family who have an interest in what happens to your business: Partners, vendors, customers not to mention employees if you have them. You may not care what happens to them, but more than likely you do and it is important to you, so they need to be part of your plan as well.

As you can see, exit planning is not something you can do in one day, you really need to spend considerable time on it. It is not something you can delegate. You are going to have to do it yourself, so delegate something else and get started. It is more important than most people in their 20's, 30's and 40's think.

Retirement planning is hard, but fortunately, there is plenty of help available. Most are for employees and most deal with the financial aspect of retirement. This one also deals with the very important mental aspects. Financial security alone does not necessarily make you happy. There is more to it than that. This book helps with that.